2-1 Buydown and How It Helps You

2-1 buydowns are a popular topic that some sellers and buyers may consider to increase sales opportunities. A 2-1 buydown program is usually offered by sellers as concessions to incentivize buyers. A 2-1 buydown essentially allows borrowers to make a lower mortgage payment for the first two years of their loan, and payments go back up on the third year of the loan. The 2-1 buydown is also called a “temporary” buydown because the impact is scheduled to end on a set payment plan. Think of it as easing into mortgage payments over time

If you’re thinking of buying and the interest rates have you worried about the potential for purchase power you might consider the 2-1 buydown as a way to reduce your monthly mortgage payment. Let’s explore exactly what a 2-1 buydown is, how it works, and the pros and cons you will consider.

What is a 2-1 Buydown?

A 2-1 buydown program is a type of financing offer to reduce your interest rates for the first two years of a mortgage. If you select the 2-1 buydown that means that as a buyer your monthly payment is recalculate as tho your interest rate was reduced by 2% the first year and 1% the second year.

By the third year of the mortgage term, the interest rate is fully calculated into your payment. But with a 2-1 buydown, buyers have reduced payments for the first two years.

How does a Temporary Buydown Work?

A temporary buydown is a seller paid concession available for primary home purchases (and some secondary home purchases). It enables borrowers to have a lower interest rate for the first two years of purchase and ease into their mortgage payments.

The seller funds the temporary buydown through concessions (seller paid) into a specific escrow account, but it must be included in the purchase contract and negotiated by the real estate agent through the process.

The total sum of the 2-1 buydown, or temporary buydown, is held in a custodial escrow amount and is applied to the buyer’s payment. The buyer will have a reduced monthly payment, and the difference in interest rates comes out of the escrow account. The first year, the interest rate is lowered by 2 percentage points and 1 percentage point the following year.

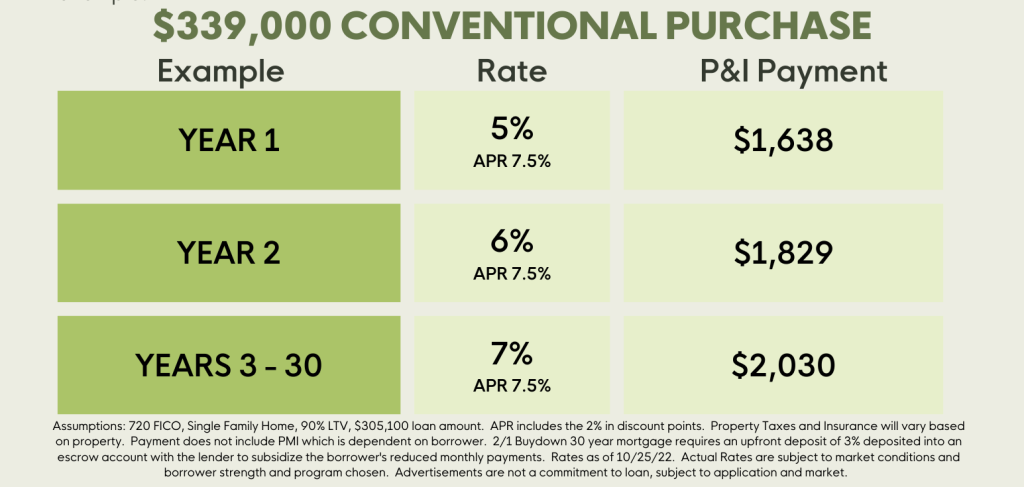

Temporary Buydown Scenario

Here is a simple scenario to consider the 2-1 buydown program and it’s impact to you as a buyer.

So you’re buying a $339,000 house with a 10% down payment for a mortgage loan of $305,100 and an interest rate of 7% and APR of 7.5%. A monthly principle and interest (P&I) payment would be about $2,030 approximately.

With a 2-1 buydown, your APPLIED interest rate would decrease by 2% from the original rate payment for the first year (or 12 months). So, with a 5% interest rate, your monthly P&I amount would be $1,638.

The following year, your APPLIED interest rate would be reduced by one percentage point from the original rate, taking it to 6%. The monthly P&I amount you’d be paying would be $1,829.

On the start of the 3rd year of payments (month 25) your payment would then be at the original 7% interest rate from the third year onwards, taking your monthly P&I back to $2,030.

Keep in mind that this scenario doesn’t factor in taxes and insurance, so your actual monthly payment amount will vary by location and needed Mortgage Insurance, but you can see the difference between years 1 and 2 versus year 3 and after. Running these different scenarios can help you better forecast what you’ll be paying for the first 2 years versus the third year onwards to understand if it’s the right decision for you.

Pros and Cons of a Temporary Buydown?

The first thing to point out with a temporary buydown is just that, it’s temporary. Initially, it can be a pro that you’re paying lowered mortgage payments the first two years. However, if your income doesn’t match the payment amount in the third year of the loan, it can become a serious con. That’s why it’s essential to consider the impact of the monthly payments once they resume at the original interest rate from the third year onwards.

A temporary buydown can benefit both sellers and buyers, but it’s more likely to occur in a buyers’ market where there are many properties available but not enough buyers. For buyers, this is a bridge for a market with high rates and gives them an opportunity to buy now, when interest rates are high, with the ability to refi later if rates go down. If they don’t go down and continue to go up, then at least they’ve locked in a lower rate right now. For sellers, it enables them to move properties faster and keeps them from staying on the market too long. For buyers, the reduced monthly payments can help manage initial housing expenses.

Better to do a Temporary Buydown or buy the rate down forever?

There are some crucial differences between a temporary buydown and buying down the interest rate. With a temporary buydown, it’s just that – temporary. You’ll lower the interest rate for a short period of time, but borrowers pay the regular interest rate moving forward on the loan.

However, buying down the interest rate means borrowers pay an additional charge to receive a lowered interest rate. Buying down the interest rate is useful for reducing your long-term interest rate and monthly payments. But it can also greatly reduce your cash reserves for moving and unplanned expenses when owning a home.

Whether you choose to do a 2-1 buydown or buy down the interest rate will depend on first if you qualify for the mortgage loan at the regular interest rate. Then how much money you’re willing to invest short-term and long-term for your home and what your income will look like over time. So before deciding, it’s crucial to run the figures for both scenarios to understand what will be most beneficial to you initially and in the long term.

___________________________

*The sample rates provided are for illustration purposes only and are not intended to provide mortgage or other financial advice specific to the circumstances of any individual and should not be relied upon in that regard. Be My Neighbor Mortgage cannot predict where rates will be in the future. The payment example does not include assessments. Actual payment obligations may be greater and may vary. Mortgage Insurance Premium (MIP) is required for all FHA loans and Private Mortgage Insurance (PMI) is required for all conventional loans where the LTV is greater than 80%. Rate(s), APR(s) and payment info is valid as of 10/25/2022 and assumes a first lien position, 720 FICO score, 25-day rate lock, based on a single-family home. All terms are subject to change without notice. Loans are subject to underwriting guidelines and the applicant’s credit profiles, not all applicants will receive approval. Available for conventional, FHA, VA, and USDA loans only.